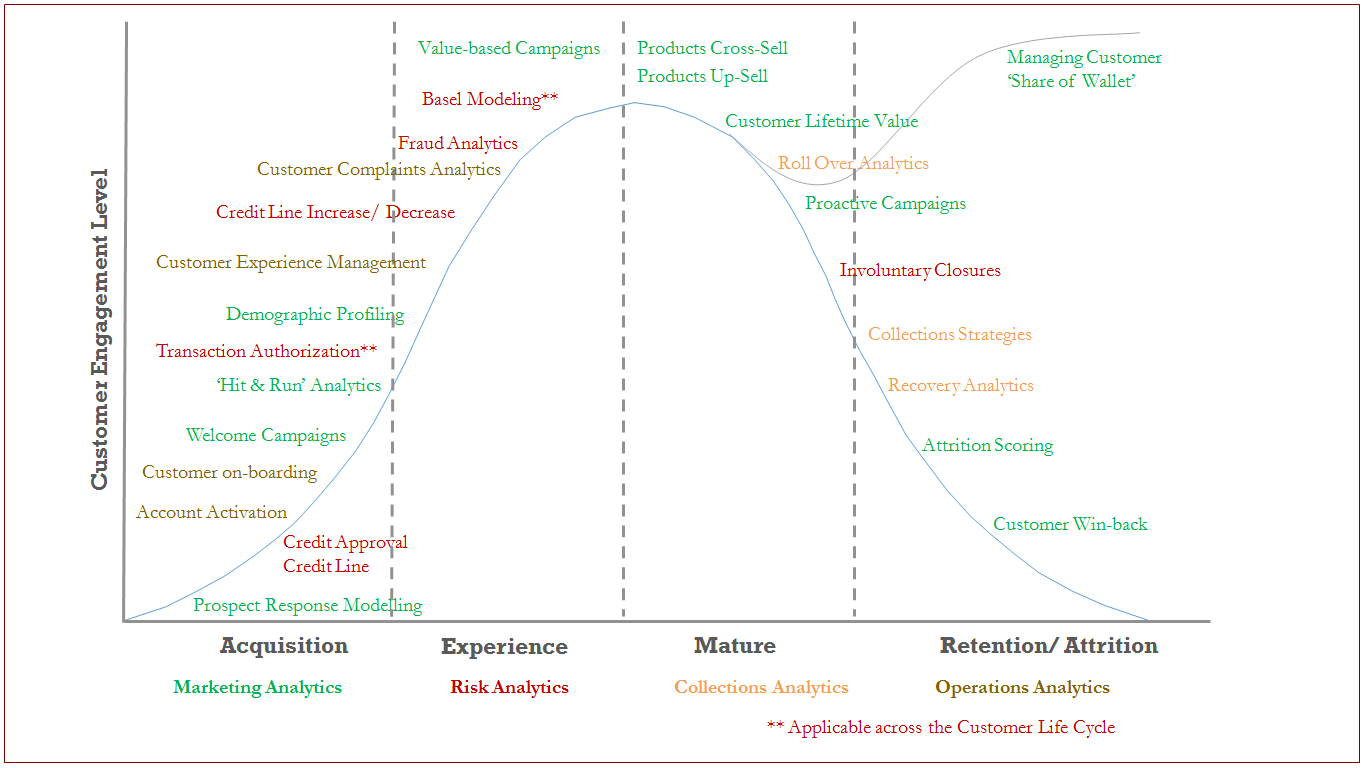

Banking

insAnalytics provides a range of data-driven solutions for our Banking clientele across the industry landscape – consumer banking, wealth management, corporate banking, and investment banking. We leverage our cross-functional expertize across banking operations, customer experience, marketing and risk management to provide technology-agnostic and cost-effective business solutions to our Banking clients. We design & deploy end-to-end business solutions in the areas of customer acquisition, share-of-wallet analysis, churn prediction, credit scoring, collections, loss forecasting, stress testing, fraud identification, and many more.